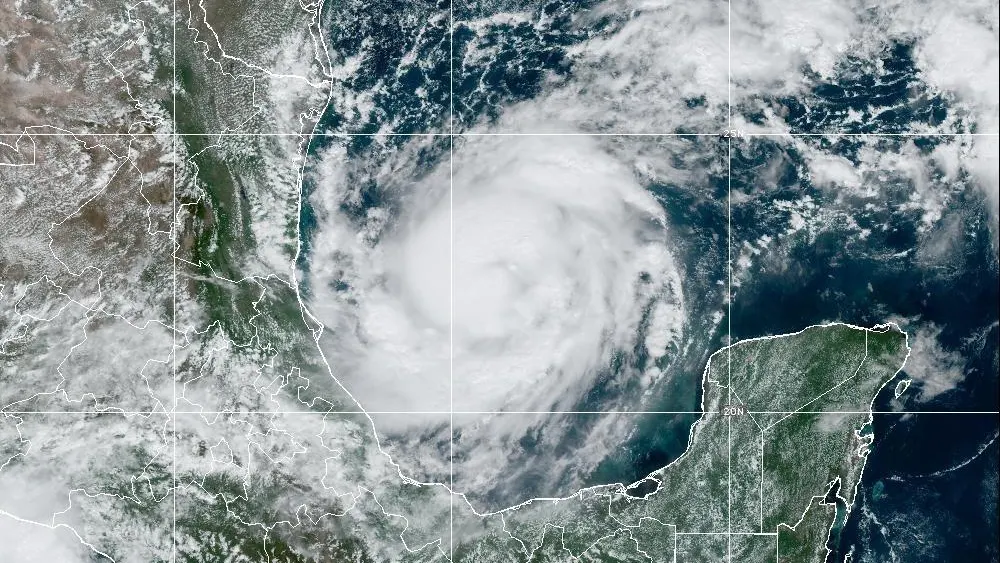

Our thoughts are with our teams, clients, and community in Florida as Hurricane Milton has impacted the region. We are deeply thankful for all the first responders and everyone working tirelessly to help those in need during this challenging time.

In the event that there is any damage to your property, please call your carrier directly. For a complete list of our carriers in Florida and their phone numbers to file a claim, click here.

In the event that you need to report a claim, please read the tips below:

Locate you declarations page for each of your insurance policies. (The first page of your policy that usually shows the policy number and effective dates.)

If damage occurs, take photos.

Contact your carrier or insurance agent to file a claim as soon as possible.

Save the list of carriers and phone numbers to file a claim to have on hand.

We understand the stress and uncertainty that comes with severe weather events. Our thoughts are with all those who may be affected by Hurricane Milton. If you have any questions, please call one of our Florida locations.

This content is for informational purposes only and not for the purpose of providing professional, financial, medical or legal advice. You should contact your licensed professional to obtain advice with respect to any particular issue or problem. Please refer to your policy contract for any specific information or questions on applicability of coverage.

To effectively navigate the ever-evolving landscape of workers’ compensation in New York State, it’s crucial to understand the changes to the state’s Experience Modification Factor (MOD). In our recent Risk Management 101 webinar, Megan Coville, Director of OneGroup’s Risk Management Department, provided a comprehensive overview of these changes and their impact.

What is an Experience MOD?

The MOD is a critical metric that measures safety performance and claims management. Essentially, a MOD is a “safety score” that compares expected loss rates to actual losses over a three-year period. This calculation can significantly impact workers’ compensation premiums, with higher MODs leading to higher costs.

Key Changes

One of the recent key changes was New York’s departure from the National Council for Compensation Insurance (NCCI) in 2022. The state has now developed its own equation for calculating the MOD, focusing on New York-specific class codes and experience loss rates. This shift aims to better reflect the unique risks and challenges faced by businesses operating within the state. Understanding the split point, a variable factor that determines how claims are weighted in the MOD calculation, is also crucial.

Effectively Manage Your MOD

Prevention and proactive risk management strategies are essential to control the experience MOD. This includes knowing industry-specific exposures, reviewing data, and implementing measures to mitigate risks like slip and falls, ergonomic issues, and overexertion. Timely reporting and documentation of claims, as well as effective return-to-work programs, can also help maintain a low MOD and avoid premium increases.

Ultimately, it’s important to regularly review your workers’ compensation claims and MOD status. By understanding and adapting to these changes, you can better manage your workers’ compensation costs and maintain a safer workplace.

For more information or to discuss how these changes impact your business, please reach out to OneGroup. Our specialists are here to help you navigate the complexities of New York’s workers’ compensation system and ensure you’re making informed decisions. Contact us today to learn more!

This content is for informational purposes only and not for the purpose of providing professional, financial, medical or legal advice. You should contact your licensed professional to obtain advice with respect to any particular issue or problem. Please refer to your policy contract for any specific information or questions on applicability of coverage.

Please note coverage can not be bound or a claim reported without written acknowledgment from a OneGroup Representative.

Warehouses can be dangerous places. Speed and efficiency are vital, which means moving vehicles, heavy foot traffic and goods flowing in and out.

Your warehouse employees can easily fall victim to injuries. Practicing safe habits and knowing what dangers to avoid will keep your employees out of harm’s way and your warehouse safe.

Keeping workers safe

Your goal as the business owner is to provide a workplace free of injuries and accidents.

The first step is to set a minimum safety standard for all practices and operations. By setting clear minimum safety standards, you are actively working toward preventing injuries and illnesses and reinforcing that safety is the priority.

Employees should always be aware of their surroundings. Train them on safety during onboarding and periodically after that to remind them of the safe practices they learned upon hiring.

Warehouse supervisors and managers should ensure safety procedures are posted clearly near equipment and hazardous areas. These postings provide visual reminders of the dangers associated with workers’ jobs and the safety precautions they should take to avoid injury.

Hazards

Warehouses are full of hazards, some more obvious than others. Awareness of common hazards helps keep employees safe and prevent damage to products.

Warehouse hazards that need particular attention are:

Slips, trips and falls: Wet floors, oily spills, ice, mud, clutter and poor visibility all contribute to slipping hazards. An employee can also fall if they climb a rack or get on a forklift to retrieve a product. Provide employees with fall protection whenever they are working more than 4 feet off the ground.

Forklifts: Employees are severely injured or killed every year while operating forklifts. Turnovers account for a high percentage of the fatalities.

Loading docks: A person can get injured if a forklift runs off a dock. They can also get hit by falling objects or moving equipment.

Conveyors: Workers can get caught in pinch points or hit by falling products. They can also sustain injuries from using repetitive motions.

Equipment hazards

Heavy equipment such as forklifts, hydraulic dollies and hand jacks should be used with precision and precaution, and only after proper training. Below are some important safety practices for equipment:

Train, evaluate and certify all operators to ensure they can operate forklifts safely.

Properly maintain haulage equipment, including tires.

Before using a forklift, examine it for hazardous conditions that would make it unsafe to operate.

Maintain sufficient clearances for aisles, loading docks and passages where forklifts are used.

Ensure adequate ventilation to keep noxious gases from engine exhaust below acceptable limits. You can do this by opening doors and windows or using a ventilation system.

Don’t handle loads that are heavier than the weight capacity of a forklift.

Watch out for pedestrians and other vehicles, particularly around aisles.

Use lift trucks with reinforced bumpers.

Make sure any accessories you use are compatible with the equipment.

Report, tag as “Out of Service” and remove defective equipment from service until it’s repaired.

Test equipment controls and functionalities before starting a job.

Electrical hazards

Electrical tools, cords and equipment are integral parts of the warehouse floor, and all pose serious threats if handled carelessly. Enhance electrical safety at your warehouse by addressing the following areas of concern:

Use appropriate grounding. Ensure all electronic equipment is appropriately grounded. This will decrease the risks of electrical shocks. Provide ground fault circuit interrupters for receptacle outlets. Also, make sure power cords are not blocking aisles or walkways to prevent trips and falls.

Maintain optimal condition. All electrical equipment should be in optimal condition. Outlets and cords should be in good state with no exposed or frayed wires. Regularly inspect electrical tools with preliminary checks and appropriate tests. Carry out periodic preventive maintenance and look for visible signs of damage or flaws. Visual inspection is one of the most basic steps to ensure electrical safety.

Avoid water. This may seem obvious, but you should keep electrical equipment away from water. Completely power down equipment when not in use, during service and during cleaning. Areas surrounding electrical cords and equipment hold high potential for electrical hazards. Keep these areas clean and dry. Keep materials such as metals and water out of these areas as an added precaution.

Invest in training. Electrical safety training is one of the most important steps any warehouse manager can take to safeguard the facility.

Chemical hazards

Chemicals can be dangerous. Some chemicals present risks anytime you use them, while others are only dangerous if handled improperly. Substances that start relatively safe can become hazardous over time. For example, ether can degrade into peroxide after it’s been stored for about a year. And peroxide is explosive.

Every organization that uses or stores chemicals should have a control system. All containers should be labeled with their contents and expiration dates.

You also need a material safety data sheet for every chemical you use. Train employees who handle these materials on proper use, storage and disposal. All employees need to know what to do in the event of a spill, a chemical burn or another accident.

Safety and training

Safe warehouses continually train employees on safety precautions and protocols. Include regular, frequent updates and refresher courses in your training program. And make preventing unsafe behaviors your No. 1 priority.

Proper handling/lifting

Handling materials, whether by powered equipment or manually, can cause injuries to hands, fingers, feet and toes. And improper lifting or overexertion can lead to back injuries.

Whether employees use power equipment or their own bodies to move materials, they should obey these handling and lifting safety rules:

Make preparation the first step. Check the load to decide how best to move it. Check the route to make sure there are no obstacles in the way. And check if there’s space for the load at its destination.

Always use safe lifting techniques. Use your legs and keep your back in a natural position while lifting.

When carrying objects, be sure you can see over the load.

Don’t twist while carrying a load. Instead, shift your feet and take small steps in the direction you want to turn.

When using material-handling equipment, follow proper operating procedures.

When using a hand truck or pallet jack, load heavy objects on the bottom and secure bulky or awkward items.

Push, rather than pull, manual material handling equipment whenever possible. And lean in the direction you’re going.

Personal protective equipment

Personal protective equipment (PPE) refers to clothing and equipment meant to ensure the safety of employees working in a warehouse environment. Common PPE for warehouse workers includes:

Hard hats

High-visibility safety jackets

Safety goggles

Warehouse safety boots with steel toe caps

Overalls

Safety gloves

These items can vary depending on the work environment.

Be sure to have spare PPE readily available for visitors and infrequent employees, as well as spares for regular employees.

Communication and signage

Safety signs in your warehouse are highly important to protect your workers and visitors from injury or even death. If you implement effective, clear visual communication, you’ll likely experience fewer accidents and injuries, increased efficiency and safer behavior throughout your facility.

Signage also allows you to communicate with workers even when a supervisor isn’t immediately present.

Your safety signage must be professionally manufactured, compliant with safety regulations and readable by all workers. And you must post your signage in the right locations, including entrances, exits and whererever equipment is located or moved to.

Security

Maintaining security at your warehouse is important if you want to keep your employees and the facility safe. Due to high volumes of inventory, warehouses are often at high risk for burglary and theft, especially if the inventory is highly valuable.

Risks to the security of your warehouse can be both internal and external sources. Internal security threats can come from employees and third parties hired by the business, while external security threats would involve anyone else who enters the warehouse without authorization.

To reduce your risks, consider the following:

Visitor sign-in procedures. Establish a visitor registration process to identify everyone who enters the warehouse. Don’t allow visitors or delivery drivers to go through the warehouse unaccompanied.

Building access. Install a barrier such as a fence around the exterior yard of the warehouse. Keep the gate locked when the warehouse is closed. If necessary, risk managers may allow access to authorized employees.

Activate alarms on all doors, including emergency exit doors, when the warehouse is closed.

Electronic security and surveillance systems. Use an electronic system to control access to high-value rooms and cages. Your access control system should provide an audit trail of who enters, when and for how long.

Install a video surveillance system to record activity in high-value cages and rooms. Place your cameras to view entrance points as well as interior areas.

Install intruder alarms to enable a fast and coordinated response in the event of theft or vandalism.

Employee screening. Employee theft can create staggering losses within warehouses. Conduct thorough background checks of potential employees before hiring, and pay attention to any accounts of theft or unexplained warehouse job losses.

Set up an anonymous reporting system. This will allow employees to report a coworker they believe is stealing without fear of repercussion.

Maintain a safe, productive warehouse

A safe warehouse is an efficient and productive warehouse. Provide training on hazard awareness, safety inspections and safety measures. This can help maintain a safe and secure working environment.

Businesses in the warehousing industry need insurance with adequate coverage for various liabilities. Contact our Risk Management team to learn more about essential policies and risk management strategies for your warehouse.

This content is for informational purposes only and not for the purpose of providing professional, financial, medical or legal advice. You should contact your licensed professional to obtain advice with respect to any particular issue or problem. Please refer to your policy contract for any specific information or questions on applicability of coverage.

Please note coverage can not be bound or a claim reported without written acknowledgment from a OneGroup Representative.

Did You Know? Medicare’s Annual Enrollment Period (AEP) Begins on October 15th

Are you or a loved one enrolled in Medicare? It’s important to be prepared for the Annual Enrollment Period (AEP), which begins on October 15th and runs through December 7th. This is a key time for Medicare beneficiaries to review and update their plans to ensure they have the best coverage.

What is AEP?

The Annual Enrollment Period is when you can:

Enroll in or switch Medicare Advantage Plans (Part C).

Join, switch, or drop Medicare Prescription Drug Plans (Part D).

Return to Original Medicare (Part A and Part B) from a Medicare Advantage Plan.

How to Prepare:

Review Your Coverage: Check if your current plan still meets your needs, considering any changes in your health or medications.

Compare Plans: Look at the options available in your area, focusing on coverage, costs, and any changes for the upcoming year.

Check Provider Networks: Make sure your preferred doctors, hospitals, and pharmacies are in-network.

Evaluate Prescription Coverage: Ensure your medications are covered and check for any changes in co-pays or coverage.

Seek Advice: Reach out to Medicare professionals at OneGroup for personalized guidance and informed decisions.

What to Expect:

During AEP, you might receive a lot of information from different Medicare plans. It can be overwhelming, but don’t worry! Here’s what you can expect:

Plan Notices: Your current plan will send you an Annual Notice of Change (ANOC) detailing any changes for the upcoming year.

Marketing Materials: You’ll likely receive brochures and flyers from various Medicare plans highlighting their benefits.

Increased Communication: Expect more emails, calls, and advertisements about Medicare plans. Use this information to compare and make informed decisions.

By following these steps and knowing what to expect, you can confidently navigate the AEP and secure the best coverage for your needs. We’re here to help you every step of the way.

For more information

To learn more about our Medicare solutions and receive complimentary help, click here.

We are not a government agency. We are licensed insurance agents who discuss insurance programs such as Medicare Advantage, Medigap, and Medicare Part D Prescription Drug Coverage. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all of your options.

This content is for informational purposes only and not for the purpose of providing professional, financial, medical or legal advice. You should contact your licensed professional to obtain advice with respect to any particular issue or problem. Please refer to your policy contract for any specific information or questions on applicability of coverage.

Please note coverage can not be bound or a claim reported without written acknowledgment from a OneGroup Representative.

Most brokers earn commission from insurance carriers. Others charge fees for services provided. Greater transparency in these payment methods can help you control rising health care costs.

But, more importantly, a clear picture of how your broker is paid can lead to a long-term, strategic relationship that benefits you and your employees.

Working with a broker is often the first step in creating a comprehensive employee benefits plan. Your broker can help you:

Choose the right carriers

Implement the best coverage for your employees

Manage costs

Complete open enrollment

Educate new employees about their choices

Resolve issues throughout the year

What does your broker get out of the deal? Have you ever thought to ask what’s in it for them?

Asking the hard questions

Every broker should be able to answer these questions:

Will you push me to use certain insurance companies because they pay you more?

Will you charge any fees in addition to the monthly premium?

Will I receive a monthly bill from you in addition to the one I already get from the insurance company?

Will you push me to use certain insurance companies because they pay you more?

The answer to the first question should always be a resounding NO. Brokers should place business with the carrier that is in the best interest of their client.

Be sure to ask for a monthly reconciliation of all commissions paid to your broker by insurance carriers. It will allow you to see exactly where your premium dollars are going and how your broker is being compensated. It will also enable you to see if the carrier is creating incentives for your broker to encourage participation and reduce overall costs.

Will you charge any fees in addition to the monthly premium?

Some brokers charge a monthly fee to manage your plan. In most cases, this fee covers the cost of online benefit portals, a dedicated customer service team and ongoing employee education. Be sure to get in writing what services your broker will provide and when. Negotiate a per-employee rate and make sure that rate is locked in for at least 12 months.

If your broker does not offer any services other than placing coverage, there should be no additional fees.

Will I receive a monthly bill from you in addition to the one I already get from the insurance company?

If your broker charges a monthly fee, you should receive a bill for the services provided. Each month, you should receive an itemized list of active employees and any adjustments for terminations and new hires.

If your broker bills consulting fees for certain services, like a salary survey or dependent audit, those items should be listed separately. In many cases, you will receive a separate bill altogether.

Commission-based models

Most insurance companies pay relatively the same commission to brokers in a certain geographic area. That means if your company offers a fully insured health care plan that is qualified under the Affordable Care Act, your premium should be the same no matter which broker you choose.

If you have a self-insured health care plan, the administrative fee you pay can fluctuate and influence the amount of commission your broker earns. Many brokers will accept a lower commission in order to save their clients money on administrative fees.

Some insurance companies will also pay brokers a flat fee per policyholder. For example, each month in the first year of the plan, the broker will receive an additional $15 per new enrollee. If you stay with the same carrier in subsequent years, the rate will go down. For example, the broker may receive an additional $7.50 each month per renewal.

Fee-for-service models

Today’s brokers take a consultative approach with their clients. Some charge one-time fees for particular services such as creating an employee handbook or drafting a five-year strategic benefit plan. Others charge a larger fee, like a retainer, to examine your employee benefits plan and make recommendations on cost-saving programs and implementation.

To make the most of these fee-for-service models, your broker should be willing to sacrifice a portion of the fee based on how well their recommendation works. For example, your broker may be willing to return a percentage of their fee if your plan doesn’t meet the projected cost savings.

Transparency is key

If you have any questions about how your broker’s pay is structured, ask. No matter how your broker is paid, they should be open and honest about how they make their money. For additional information, contact our Employee Benefits team.

This content is for informational purposes only, should not be considered professional, financial, medical or legal advice, and no representations or warranties are made regarding its accuracy, timeliness or currency. With all information, consult with appropriate licensed professionals to determine if implementing any recommendations would be in accordance with applicable laws and regulations or to obtain advice with respect to any particular issue or problem.

Preventing slips, trips, and falls in municipal settings involves a proactive approach with fall protection, housekeeping, and regular maintenance to ensure a safe working environment.

In municipal settings, ensuring the safety of employees and the public is paramount. The Occupational Safety and Health Administration (OSHA) requires fall protection whenever employees are working at an elevation of 4 feet or more. This can include guardrails, harnesses, and other safety measures. However, slips, trips, and falls can occur at any height, often due to inadequate housekeeping or distractions.

How to Prevent Slips, Trips, and Falls in Municipal Workplaces

Here are some prevention techniques to help keep municipal employees and the public safe:

Reduce Distractions

· Limit cell phone use in active work areas.

· Observe employees for signs of illness, excessive stress, or other impairments.

Prioritize Housekeeping

· Ensure work surfaces and floors are clean and orderly.

· Address water, chemical, and equipment leaks immediately.

· Remove or route hoses, cords, and other obstructions away from walkways and emergency areas.

Use Fall Protection

· Use portable ladders and elevated work surfaces with handrails.

· Train employees on the proper use of harnesses and lanyards.

Regular Maintenance

· Schedule regular preventive maintenance for equipment to prevent leaks and breakdowns.

· Ensure tools and equipment are returned to proper storage areas after use.

Clear Signage

· Post clear signage wherever floor conditions change (e.g., dry to wet).

Employee Training

· Train employees on how to safely perform tasks and identify hazards.

· Conduct walkthroughs to identify and address potential hazards.

· Encourage employees to report hazards and suggest improvements.

Following these prevention techniques will help protect your workforce and the public, reduce liability, and ensure compliance with safety regulations. By prioritizing slip, trip, and fall prevention, you can create a safer environment, enhance productivity, and foster a culture of safety.

Contact Us

To learn more about unique municipality risks and how to address them, contact our OneGroup Municipality team.

This content is for informational purposes only and not for the purpose of providing professional, financial, medical or legal advice. You should contact your licensed professional to obtain advice with respect to any particular issue or problem. Please refer to your policy contract for any specific information or questions on applicability of coverage.

Please note coverage can not be bound or a claim reported without written acknowledgment from a OneGroup Representative.

A lot of condo owners assume that their association takes care of insurance, in addition to maintenance. But that’s not entirely true, especially when it comes to your belongings and other items within your unit.

What does your condo association cover?

Condominium associations are usually responsible for insurance and upkeep when it comes to building exteriors and communal amenities. Your association probably insures the interior of the building as well, up to and including the walls of your unit.

But what about things inside or attached to those walls? Well, it’s your responsibly to protect those.

Your association probably has “bare walls” coverage, which leaves unit owners like you responsible for all property and fixtures in individual units.

“As built” coverage makes it the owner’s responsibility to insure any upgrades or additions made to the original dwelling.

What’s covered by most condo owners policies

Personal property damaged by storms, accidents, theft or loss

Alternative lodging and required transportation if your condo becomes uninhabitable due to a covered event

Liability protection if you are held financially responsible for loss of or damage to another person’s possessions, or the costs associated with someone else’s injury

What’s not covered by most condo owners policies

Standard maintenance

Wear and tear and associated damage

Effects of termites, insects, birds or rodents

Rust, rot or mold

Liability due to malicious, dishonest, criminal or illegal acts

Upgrade your protection options

The following coverages can be added to your policy by optional endorsement:

Vacant condo coverage for damages that occur in a unit left vacant for 30 consecutive days or more (Time is specific to each policy.)

Floods

Earthquakes

Sewer/septic backups and sump pump backups

Specialized hobby items, fine art or other high-end collections

Home office and from-the-home businesses

Credit theft protection and monitoring

Loss assessment coverage (This helps protect you if you suffer a catastrophe that exceeds the association’s limits.)

What we offer

Customizable coverages, limits and deductibles

Experience with the unique needs of condo owners who must coordinate insurance with condo association coverage

Responsive, friendly claims professionals

Easy claims reporting process and communication with your HOA

Give us a ring

Give us a call to learn more about covering the current gaps in your coverage, so you can enjoy your condo worry-free.

This content is for informational purposes only and not for the purpose of providing professional, financial, medical or legal advice. You should contact your licensed professional to obtain advice with respect to any particular issue or problem. Please refer to your policy contract for any specific information or questions on applicability of coverage.

Please note coverage can not be bound or a claim reported without written acknowledgment from a OneGroup Representative.

Crystalline silica is a common mineral found in the earth’s crust. Sand, stone, concrete and mortar contain crystalline silica.

Glass, pottery, ceramics, bricks and artificial stone are also made with crystalline silica. Crushing, drilling or cutting these minerals creates a superfine dust that people breathe into their lungs. Silica dust exposure can lead to severe health problems or death.

The Occupational Safety and Health Administration (OSHA) estimates that 2.3 million workers are exposed to silica as part of their jobs. Learn more about silica dust and ways to test for and prevent exposure.

Job duties that can cause silica dust exposure

Workers in various industries could be exposed to silica dust in their daily duties. These tasks include:

Abrasive blasting with sand

Sawing brick or concrete

Sanding or drilling into concrete walls

Grinding mortar

Manufacturing or installing brick, concrete blocks, stone countertops or ceramic products

Cutting or crushing stone

Foundry work

Drilling and hydraulic fracturing (aka fracking)

Health dangers caused by crystalline silica dust

Crystalline silica particles are tiny, at least 100 times smaller than beach sand. They might look like dust in the air, but they’re more insidious than that. Your workers could get disabling silica-related diseases if they breathe in silica dust particles, including:

Silicosis: A lung disease caused by inhaling silica particles. Over time, the particles cause inflammation and scarring in the lungs, making breathing difficult. Silicosis causes permanent lung damage.

Lung cancer: A type of cancer that begins in the lungs and can spread to lymph nodes or other parts of the body. It can develop in people with prolonged exposure to harmful substances like silica dust. Even people who have never smoked can develop lung cancer.

Chronic obstructive pulmonary disease (COPD): COPD is an inflammatory lung disease that obstructs airflow, causing symptoms like breathing difficulty, cough, excessive mucus and wheezing. Long-term exposure to air pollutants, like silica dust, can cause COPD.

Kidney disease: OSHA reports that workers exposed to respirable crystalline silica have a higher risk of developing kidney disease. Diseased kidneys filter waste from the body less effectively, and kidney disease can sometimes progress to kidney failure.

Ways to reduce silica dust exposure in the workplace

OSHA’s Respirable Crystalline Silica standard protects workers from exposure to dangerous levels of silica dust. The standard establishes a permissible exposure limit (PEL), or the maximum amount of crystalline silica a worker can be exposed to during an eight-hour shift. The PEL must not exceed 50 micrograms per cubic meter.

The standard also requires employers to prevent workers from being exposed to silica dust. Some of the prevention requirements are:

Exposure control plan

You must create a written exposure control plan. Your plan must identify tasks that increase workers’ silica dust exposure, ways to control exposure or restrict access to hazardous areas, and how you will train your employees.

Engineering controls and exposure control methods

You should use engineering controls such as water, ventilation and work methods to minimize worker exposure.

For example, a concrete drill jig vacuums silica dust as it drills into cement. The two primary components are a special drill bit and a dust collection unit. Unlike traditional drill bits, the drill bit on a concrete drill jig has a hollow center. When you drill into concrete, the bit cuts through the concrete, creating silica dust. The vacuum nozzle connects to an opening at the top of the drill bit shaft where the hollow center begins. The vacuum sucks up the silica dust and deposits it into a container. The hollow bit and vacuum combination prevent silica dust from dispersing into the work environment.

Housekeeping

You should implement good housekeeping practices to prevent the accumulation of silica dust. Prevention can include vacuum dust collection and water delivery systems to cut down on dust. Avoid dry brushing, dry sweeping or using compressed air to clean since it pushes crystalline silica dust into the air, causing an inhalation hazard.

Personal protective equipment (PPE)

Use dust masks and respirators if you can’t engineer out the silica dust exposure at your work site. Have each employee trained and fitted when you use respirators.

Employee training

Train your workers on silica dust risks, including proper PPE and ways to limit their exposure. Tell them about the health effects of silica exposure and the purpose of medical surveillance if their job duties require it.

Work site air sampling and analysis

Test your work site if crystalline silica is in the materials you use. According to OSHA, the maximum allowable amount of breathable crystalline silica in the air spread over an eight-hour total weight average (TWA) is 50 micrograms per cubic meter. Breathing in particles above this permissible exposure limit (PEL) can compromise employee safety and health.

You can assess for silica dust using a personal cyclone sampling device. Cyclones are small, lightweight devices worn on clothing. They pull air through at a specified flow rate and separate dust particles based on size. This allows them to measure the amount of silica in the environment.

You can hire a professional silica testing firm to assess the air for silica dust exposures. If you’re not clear on the monitoring techniques for your industry, a professional testing facility might be your best option. Something as simple as an incorrect flow rate can skew results so it’s important to understand the devices and how to calibrate them.

OSHA’s action level is when the airborne concentration of silica dust is at 25 micrograms per cubic meter using the eight-hour TWA. Exposures at or above this action level trigger requirements for exposure assessments and medical surveillance.

If the most recent exposure assessment reveals employee exposures at or above the action level but below the PEL, you must repeat silica exposure monitoring within six months.

If the most recent exposure assessment reveals employee exposures above the PEL, you must repeat silica exposure monitoring within three months.

Medical surveillance

If dust exposure exceeds OSHA’s action level for 30 or more days each year, you must offer medical exams. The exams must include chest X-rays and lung function tests every three years. Use OSHA’s Appendix B, Medical Surveillance Guidelines to help physicians and licensed health care professionals (PLHCP) understand the medical surveillance provisions of the Respirable Crystalline Silica standard. Appendix B is divided into seven sections:

Section 1: Silica-related diseases, medical and public health responses

Section 2: Components of the medical surveillance program

Section 3: Roles and responsibilities of the PLHCP implementing the program

Section 4: Confidentiality and other considerations

Section 5: Additional resources

Section 6: References used to create the appendix

Section 7: Sample forms for the written medical report for the employee, the written medical opinion for the employer and the written authorization

Recordkeeping

Keep records of employee training, as well as air sampling, silica exposure and medical exam results. Document your findings and the actions you took to reduce silica dust exposure.

Competent person

OSHA requires construction industry employers to designate a competent person to identify existing and predictable silica hazards. This competent person must have the authority to take prompt corrective measures.

Reassessing exposures

You must reassess for silica exposure whenever a change in production, process, equipment, personnel or work practices could result in new or added exposures.

You can read more about the OSHA standard in these publications:

Remember, the ultimate goal of the guidelines is to prevent exposure and protect workers’ health and safety. If you need help with respirable silica dust, contact OSHA’s On-Site Consultation Program for free, confidential assistance. Or hire an industrial hygienist to perform air quality testing and recommend ways to reduce silica dust.

Contact Us

To learn more about the risk of crystalline silica and how to prevent exposure, contact our Risk Management team.

This content is for informational purposes only and not for the purpose of providing professional, financial, medical or legal advice. You should contact your licensed professional to obtain advice with respect to any particular issue or problem. Please refer to your policy contract for any specific information or questions on applicability of coverage.

Please note coverage can not be bound or a claim reported without written acknowledgment from a OneGroup Representative.

The Occupational Safety and Health Administration (OSHA) can justify coming to your business for many reasons, including a random inspection

Understanding your rights and responsibilities, and how to react to a surprise inspection can help with safety operations and save you some anxiety. Use this guide to prepare for an OSHA inspection and evaluate the condition of your safety programs.

What is a random inspection?

A random inspection is simply that: random. Your facility may not have a high injury rate. Your employees may all be happy with you and the working conditions. You may not have any formal safety complaints against you. Still, you could be selected for a random inspection. OSHA occasionally conducts these inspections across industries.

You shouldn’t have much to worry about if you already practice good safety hygiene: protecting your employees from hazards, injuries and illnesses. However, neglecting safety precautions and taking chances could result in citations and fines during a random inspection.

Who conducts OSHA inspections?

Compliance safety and health official (CSHOs) are sometimes known as “compliance officers” or “OSHA inspectors.” CSHOs conduct inspections to ensure employers follow federal and state health and safety regulations. They identify potential workplace hazards, examine equipment and operational procedures, and check documentation and training records. They inspect workplace conditions, interview employees and enforce compliance with OSHA standards. CSHOs also educate employers on how to improve safety.

How OSHA prioritizes inspections

OSHA prioritizes its responses and inspections as follows:

Imminent danger (workers face immediate risk of death or serious harm)

Employee injuries, illnesses, catastrophes or death (incidents have already occurred)

Complaints from workers (not every complaint results in an investigation)

Referrals from federal, state or local agencies

Target industry inspections selected randomly (such as the National Emphasis Programs, which focus on certain hazards and high-risk industries)

Follow-up inspections (to ensure previously identified safety citations have been corrected)

OSHA gives top priority to imminent danger inspections because the employer can still prevent worker injury.

OSHA gives second priority to incidents that have already occurred so they can immediately investigate and prevent further injury.

Complaints, referrals, and targeted and follow-up inspections are conducted in order of importance.

Preparing for a random OSHA inspection

OSHA standards are a bare minimum, not the gold standard. Your safety culture should showcase more than just your compliance. It should demonstrate that you, your people and your workplace are performing well. OSHA wants proof that you comply with its requirements, but its primary purpose is to ensure you’re actively trying to keep workers safe.

If your safety culture is based on meeting compliance alone, you won’t find long-term success. You need your people’s ongoing cooperation, engagement and participation to achieve a thriving health and safety program. OSHA has the right to interview your employees during an inspection. What will a compliance officer discover during these interviews?

Tips to prepare for an OSHA inspection

In no particular order, here are some steps you can take to prepare for a random OSHA inspection:

Assess personal protective equipment

Conducting a personal protective equipment (PPE) risk assessment can help identify hazards within the general workplace and for specialized tasks.

Conduct a job hazard analysis

Conducting a job hazard analysis (JHA) for all the positions at your facility will help you rank and prioritize the hazards. This is known as your hierarchy of controls. It might even reveal hazards you didn’t think of. For example, a few workers might spot weld as part of their duties, but only occasionally. You should account for this in your safety evaluation. Provide welders with PPE, training, and a fire watch (aka spotter) when welding near combustible materials. It’s not a typical job duty, but it requires safety planning.

Develop written safety programs and action plans

Develop a safety action plan for your facility. Once you know what your hazards are and you’ve ranked their priority, you can address your safety planning, A comprehensive safety plan includes written programs like an emergency action plan and hazard communication plan. It also includes documentation such as a chemical inventory list, safety data sheets and recordkeeping.

Evaluate your employee training

Train your employees. A safety program only works if your employees understand the hazards and safety procedures available. Retrain employees periodically and whenever operations change. For example, if you adopt a new way of working or introduce new chemicals, retrain your employees. Informal toolbox talks are an effective way to communicate safety and refresh information from past trainings. It only takes a few minutes at the start of a shift. (Remember to keep records of your toolbox talks and informal on-the-job training so you can prove you’ve done it during an investigation.)

Do a mock safety inspection of your workplace

One of the easiest ways to measure your safety procedures is to do a walk-around inspection of your worksites. Engage all your employees in a mock inspection. Create a safety inspection and assign each member duties for the inspection. Front-line workers have valuable insight into workplace safety improvements. But they’ll only tell you if you allow them to speak openly, without fear of retaliation. Allow them to offer suggestions, participate in walkthrough inspections and help mitigate hazards. Consider assigning employees to sections of the worksite they don’t usually work in. They’ll have a fresh perspective and could catch safety issues that might otherwise go unnoticed.

Talk to an employment lawyer

A seasoned employment lawyer can help you evaluate your safety compliance and what to do in an inspection. Since you’ll only have 15 days to respond to OSHA’s written inspection results, connecting with an employment lawyer you trust before an inspection is best. You’ll have less anxiety knowing you already have someone to call for advice and help sorting out the details if OSHA cites you.

Model behaviors and make safety a part of every workday

Prioritize and model safety. Communicate with your employees. Give them ways to report safety concerns without fear of retaliation. Investigate near-misses and involve workers in the process. Make near-misses and safety mishaps a learning opportunity to advance safety initiatives, not a punishment. Toolbox talks serve as training tools but also allow time for worker questions and team bonding. If you make safety part of the daily routine, it won’t feel as awkward or overwhelming.

Review the safety citations in your industry

Looking into common hazards in your industry can be a learning opportunity. Review OSHA’s Top 10 Most Frequently Cited Standards. Use the list as a guide to identify and correct any items at your workplace. OSHA’s top 10 list is released annually. Many citations hold the top spots year after year. These include fall injuries, hazardous chemical exposures, and uncontrolled energy that causes unexpected machine startups and electrocution.

This repetition signals that employers can do more to protect workers in these areas.

Check other documentation and required postings

Recordkeeping

If you’re required to keep injury and illness records according to OSHA’s injury and illness recordkeeping and reporting requirements, the CSHO will request:

Your Form 300A (posted annually)

All recordable injury and illness logs

All injury and illness documentation going back five years

Don’t include personal information, such as names, in your incident report logs. Instead, anonymize the employee information before you submit it to OSHA. Use terms like “Worker 1” and cross-reference the personal data in separate files.

Posters

You’ll also need to show the compliance officer where you display your OSHA Job Safety and Health: It’s the Law poster.

Review required written safety programs

Write and maintain your written plans as prescribed in the OSHA standards. An internet search will provide tips, lists and templates. OSHA has a Sample Programs resource to help you create written programs for various hazards and industries.

You can combine your written programs into one comprehensive injury and illness prevention program (IIPP). The IIPP must address the OSHA standards that apply to the risks in your industry.

Rehearse your OSHA inspection response plan

Rehearse the OSHA inspection process with your employees. Assign key roles to your employees:

Designate someone to document what the inspector finds. Assign someone to take notes, sample (noise and air quality) and take pictures of everything the OSHA inspector mentions.

Designate people to take immediate corrective action. The CSHO might find simple infractions, like a burned-out light bulb or boxes blocking a walkway. These things are easy to correct, but you don’t want to leave the inspection walkthrough to do them. It’s best to assign a secondary team to remedy minor infractions and document them before the inspector leaves.

Designate an employee representative. If you have a union or human resources representative, make them part of the inspection. Inspectors can interview random employees. Employees have the right to talk to the inspector alone or request that a union representative be present. (It is up to the employee to decide.)

Designate a company representative. A manager should attend the inspection walkthrough and all meetings. A safety director or upper management is preferable. They should understand the OSHA standards that apply to your organization and have access to training records, injury and illness logs, and other information documentation.

Read the inspection letter. Make sure everyone on your team knows how to read an OSHA inspection letter. You team should stick to the areas the CSHO has requested to see. Don’t deviate from those areas. If you willingly allow access to areas of your business that aren’t on the inspection list, a CSHO can comment or cite what they find or see.

Rehearse appropriate responses. If a CSHO finds violations during the inspection, do not admit fault or over-explain. Simply take notes and acknowledge what the CSHO says. Tell your corrective action team to remedy the violations immediately, if possible.

If a CSHO comes to your business

A surprise inspection can be stressful, but you should never react angrily. Always be polite.

Ask to see their badge and identification number. Call the number of your state or federal OSHA office to check their credentials, including their name and badge ID. Scams involving people impersonating a CSHO have happened. (Don’t rely on the contact number on the back of the badge in case it’s a fraud.)

Usher the CSHO to a conference room or another area separate from your general work areas. Remember, any area you show them could end up in a report.

Gather your team. The CSHO will explain the reason for the inspection and the areas and documents they will inspect at the opening meeting.

Only produce the documents they request to review while on site, which may include:

Incident and injury logs and summaries

OSHA poster

Training records (five years)

Written safety programs (emergency action plan, hazard communication plan, etc.)

Safety data sheets

Chemical inventory

Medical surveillance programs and records (hearing tests, X-rays, blood samples, respirator fit tests, etc.)

Be careful about disclosing sensitive information. Remember to redact Social Security numbers and other personally identifiable information from employee records and inform the CSHO you’ve done so.

The hidden benefits of safety self-audits and inspection preparation

A massive benefit to preparing for an OSHA inspection is that you’ll increase your ability to identify hazards in the workplace. You’ll have methods to correct them before they cause an incident. You’ll gain staff buy-in that safety’s important because they’ll see you take safety seriously. Your modeled behaviors will set the pace for health and safety.

Soon, safety and wellness will be a natural part of every workday. Your workers will automatically think about safety and take action when they see unsafe behaviors. They’ll follow safe work practices and watch for safety. That’s the true purpose of OSHA: to ensure every worker gets home safely.

Contact Us

For more information please contact Matt Maguire, Regional President, North Country at MMaguire@OneGroup.com, or Todd Goodman, Risk Management Consultant at TGoodman@OneGroup.com.

This content is for informational purposes only and not for the purpose of providing professional, financial, medical or legal advice. You should contact your licensed professional to obtain advice with respect to any particular issue or problem. Please refer to your policy contract for any specific information or questions on applicability of coverage.

Please note coverage can not be bound or a claim reported without written acknowledgment from a OneGroup Representative.

A Texas court blocked the FTC’s noncompete ban, while New York enacted a law to protect freelance workers.

FTC Noncompete Ban Injunction

On August 20, 2024, the U.S. District Court for the Northern District of Texas issued a nationwide injunction blocking the Federal Trade Commission’s (FTC) final rule banning noncompete agreements. Read more here.

The rule, which was set to take effect on September 4, 2024, would have prohibited most non-compete clauses with limited exceptions for senior executives and business sales. The court ruled that the FTC lacked the authority to enforce such a ban.

As a result, the FTC’s final rule will not go into effect on September 4, 2024, and employers currently do not need to comply with its requirements.

On August 28, 2024, New York State enacted the “Freelance Isn’t Free” Act, adding Article 44-A to the General Business Law. The new law provides additional protections to freelance workers in New York State.

The law defines “freelance worker” as any natural person or organization composed of no more than one natural person, whether or not incorporated or employing a trade name, that is hired or retained as an independent contractor by a hiring party to provide services in exchange for an amount equal to or greater than $800, either by itself or when aggregated with all contracts for services between the same hiring party and freelance worker during the immediately preceding 120 days. “Freelance worker” does not include:

“construction contractors,” as defined in the Freelance Isn’t Free Act.

The law defines “hiring party” as any person or entity (other than a federal, state, or municipal governmental agency or authority) that retains a freelance worker to provide any service. Employers who utilize freelance workers are now required to put a contract in place between themselves and the freelancer. The contract must include:

An itemized list of services to be provided, and the value of those services.

The rate and method of payment.

The payment due date, which must be no later than 30 days after the completion of services.

The date the freelance worker must provide the employer with a list of services rendered under the contract.

A copy of the contract must be provided to the freelance worker, and employers must retain their own copy for at least six years. The NYS Department of Labor has developed a model contract that employers can use to meet the Act’s requirements.

Freelance workers who believe their rights have been violated may now file a complaint with the New York State Attorney General.

This content is for informational purposes only and not for the purpose of providing professional, financial, medical or legal advice. You should contact your licensed professional to obtain advice with respect to any particular issue or problem. Please refer to your policy contract for any specific information or questions on applicability of coverage.

Please note coverage can not be bound or a claim reported without written acknowledgment from a OneGroup Representative.